![]()

2.2.7 Financing of waste management

(a) Budgeting for waste services

The Municipal Systems Act, Act no. 32 of 2000 (Chapter 8, ss73-86A) requires that municipalities must ensure proper budgeting in order that they are able to deliver on their Constitutional mandate with regards to the provision of waste services. In order for a municipality to successfully implement its IWMP, it is important to establish the current available resources in terms of finance; human resources, technical skills to deliver on the municipality's mandate and to implement the goals and targets contained in the plan i.e. development of by-laws and lastly, funding for operational and maintenance costs for equipment for the effective delivery of waste services and establishment of waste disposal facilities. Further, financial management/budgeting is key as it will assist in identifying future resource needs i.e. if there is an increase in the number of households requiring waste collection services what additional resources will be required to deliver the service. A typical budget includes the following information:

Table13: Examples of categories of waste management cost drivers

| Item | Amount per annum | |

|---|---|---|

| Collection | Transportation | R700 000 |

| Capex-purchase (vehicles) | R400 000 | |

| Maintenance | R100 000 | |

| Fuel | R150 000 | |

| Receptacles | R50 000 | |

| General | R25 000 | |

| Recyclables | R25 000 | |

| Governance | Staff (remuneration) | R1 000 000 |

| Education and awareness | R500 000 | |

| IWMPS | R500 000 | |

| Disposal | By-laws | R500 000 |

| Transfer station | R300 000 | |

| Disposal sites | R10 000 000 | |

| Acquisition of land, equipment | R5 000 000 | |

| Regulatory compliance, EIA's and licence | R5 000 000 |

Table 14: Summary of the budget

| Item | Total amount |

|---|---|

| Collection | R700 000 |

| Governance | R2 500 000 |

| Disposal | R10 300 000 |

The available income/revenue should be listed and the sources of income must also be indicated. Of importance is that a municipality should determine how much revenue is generated in a given year and it should keep record of income and expenditure for compliance reasons (MFMA).

(b) Organisational and institutional matters

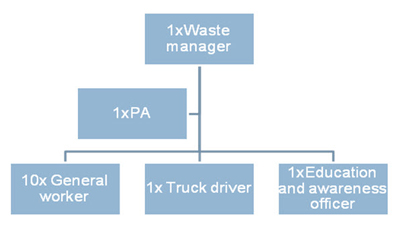

Under this section, a municipality must indicate its current organizational structure or organogram in order to determine the available human resources to deliver waste services. The organogram will highlight the number of available staff under each section such as staff to perform management duties, planning, waste collection, recycling and disposal, and enforcement etc. Further an organizational structure could potentially be used to evaluate gaps in areas where there are new functions that must be performed in order to fulfill the Waste Act's requirements. An example of an organogram is illustrated below:

Figure 3: Current organogram

If the above was an organogram of a particular municipality, then that municipality would require additional capacity in order to be able to meet the Waste Act's requirements which amongst others include the development of by-laws, enforcement of by-laws (designation of EMI's), a waste disposal facility manager to manage its waste disposal facility according to the Waste license and supervisors to supervise general workers. Staff shortages can be addressed as one of the goals/targets under the implementation plan as the successful implementation of an IWMP lies in the availability of staff to deliver on the municipality's mandate.